How can China respond to the trade war with the U.S.? By not buying U.S. treasury bonds

The U.S. and China have had a cozy business and financial relationship for the better part of the twenty first century. China was focused on an accelerated economic growth primarily driven by exports. The U.S. was focused on keeping interest rates down to fuel its debt driven economic growth. The new trade war between the two super economies will change this relationship and not necessarily for the better. The tit for tat on import tariffs is the most visible way of raging this war. However, other more stealth weapons will be used. One of them is for China to stop buying treasury bonds.

A Win-Win situation – for a long time

U.S. Federal debt holding is roughly structured as follows (source: the U.S. Treasury Department): 50% is held by the Federal Reserve and other Federal Government Agencies (yes, the government buys its own debt!), about 30% is held by foreign entities, and the remaining 20% is bought by various domestic actors (mutual funds, pension funds, insurance companies, banks, individuals, etc.). Outside the U.S. government, China is the largest single entity buying and holding U.S. treasury bonds (hence helping to finance U.S. deficit). China’s share of U.S. debt holding has significantly increased over the last two decades; reaching $1.19trn today and becoming the largest foreign holder of U.S. treasury bonds – ahead of Japan ($1.04trn and declining). By comparison, in early 2000 China held less than $100 billion in U.S. treasury securities. China’s hunger for U.S. bonds was fueled by:

- The need to place its growing commercial surplus in a risk-free financial vehicle.

- The need to keep its currency valuation lower vis-a-vis the dollar by continuously buying U.S. dollars.

The U.S. treasury securities were a perfect vehicle for China, since they allowed the country to achieve both objectives. It was also a win for the U.S., since it provided the American government with cheap financing, keeping interest rates low and thus boosting the economy thru increased government spending financed by cheap borrowing (especially needed to overcome the great recession of 2008.) In addition, the economic growth was further helped by banks’ increased funding available to the private sector, which would have been diverted to buying bonds had interest rates been higher.

Thus, for the better part of the last two decades, China was happy buying bonds and the U.S. was happy selling them to China.

Trading countries don’t (shouldn’t) go to war with each other

The escalating trade war initiated by the current administration may very well change this cozy relationship. China may stop buying U.S. treasury securities as an indirect retaliation. China’s intent will be to increase the economic cost on the U.S. The American Treasury may be forced to increase interest rates to finance a growing deficit. And this is happening when the U.S. needs to borrow more – a lot more.

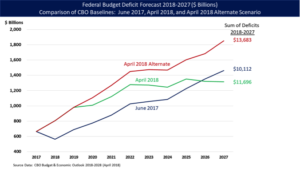

Last year’s tax cuts and spending boost will significantly increase the U.S.’ borrowing needs. According to the Congressional Budget Office, the budget deficit for the fiscal year 2018 (October 1, 2017 thru September 30, 2018) is projected to reach $804 billion. Even worse, the budget deficit for 2019 is projected to be around $1trn. Without the tax cuts and spending increase recently passed, the budget deficit was projected to be around $580 billion for fiscal year 2018 and around $650 billion for fiscal year 2019. Thus, the tax cuts and spending increase added over $550 billion to the borrowing need.

Timing is playing in Chinese favor. China withholding bond purchases may prove to be a powerful weapon, since it may force the U.S. Treasury to increase interest rates on future bond offerings in order to attract other buyers (there is no single buyer as large as China) at a time when the U.S. can least afford it. This will lead to dearer dollar, which in turn may partially reduce the impact of increased tariffs on Chinese goods. China on the other hand may opt to buy other sovereign government bonds – mostly European bonds, or finally decide to invest in growing their domestic demand to offset the effect of higher tariffs on its exports.

Lose – Lose

In trade wars as in their military equivalents, one knows how they begin, but one never knows how they will end. And the unintended consequences become their most dire results. This trade war with China will not be any different. In this war, while the U.S. holds the advantage on tariffs, China has other significant weapons in its arsenal.

Recent Comments